In a previous article, I gave an overview of three companies that benefit from increased volatility: Virtu (VIRT), Flow Traders (OTC:FLTDF) and ABC Arbitrage (ABCA:FP).

This follow-up is dedicated to ABC Arbitrage, a small-cap foreign stock which presents some interesting characteristics for investors looking to diversify their portfolios and sleep well at night during a recession.

What is "antifragile"?The concept of antifragility was developed by Nicholas Nassim Taleb in his book Antifragile. When submitted to stress, an object will usually either be harmed, or withstand the shock. But there exists a third possibility: that the object will actually benefit from being stressed.

This possibility has traditionally been underestimated, to the extent that no adjective exists in the main languages to characterize the concept. That��s why Taleb created the neologism ��antifragile�� to qualify things that gain from stress and disorder.

Nature provides many examples of anti-fragility. The human body itself is - up to a certain point - antifragile: a workout will stress your muscles and contribute to make them stronger. Human life can display elements of antifragility, as in Nietzsche��s famous line: ��what does not kill me makes me stronger.��

In the field of investments, companies get stressed in a recession. Some suffer from it, others (e.g. consumer staples) show some resilience, and a very small number of companies actually benefit. ABC Arbitrage is one such antifragile company.

ABC Arbitrage��s operationsABC arbitrage was founded in 1995 and is headquartered in Paris, France, with offices in Paris, Dublin and Singapore. It does not trade on North-American exchanges, but most brokers should be able to provide access to Euronext (SBF exchange) where the stock is listed. ABC Arbitrage has a market capitalization of ��400m at current share price of ��6.9.

As the name indicates, the company is specialized in arbitrage opportunities in financial markets, such as:

Liquidity arbitrage: detecting and correcting differences in trading prices between linked assets. Risk arbitrage: taking advantage of risk mispricing in capital markets. Statistical arbitrage: pair-trading within an industry, lead-lag effects (e.g. interaction between commodity prices and inflation). Derivatives arbitrage: detecting mispricing in options and other derivatives.(Source: company��s website)

To seize such arbitrage opportunities in financial markets across the world, ABC Arbitrage relies on proprietary algorithms. Unsurprisingly, the workforce is predominantly made of engineers and finance specialists.

ABC Arbitrage manages both its own funds and external funds. As a result, the company has two sources of income: trading revenue from its proprietary trading, and fees charged to external clients.

ABC Arbitrage is almost a pure play on volatilityABC Arbitrage displays its antifragile characteristics in volatile markets. The more stress, the more mispriced assets that the company can take advantage of. In this recent interview (in French), CEO Dominique Ceolin confirmed that volatility remains the main factor explaining the company��s performance, to the extent that shareholders can predict future results by following the VIX (or the VIX-tracking VXX).

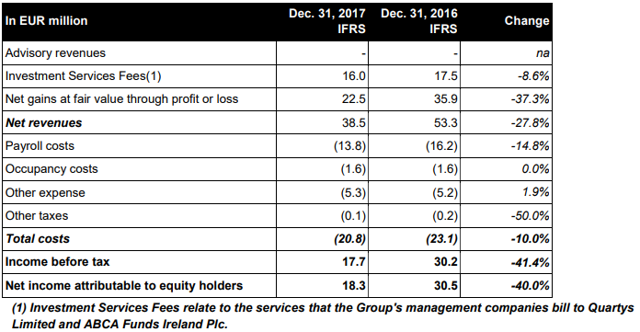

Unsurprisingly, 2017, especially the second semester which was marked by record-low volatility, was a challenging period for ABC Arbitrage. Trading revenue (included within ��net gains at fair value�� below) took a hit, and investment services revenue suffered, to a lesser extent.

(Source: company��s 2017 annual report)

Despite these ��crash-test�� conditions, the company still managed to turn an ��18.3m profit equating to a ROE of 11.5%, achieved with no leverage as the company is debt free. The decrease in payroll costs results from the substantial variable component of employees�� remuneration (30%). It does not come from cost cutting - I consider this a good thing as the company takes a long-term view. Its focus is on developing new algorithms tailored for low-volatility environments, as part of a ��Step Up 2019�� plan announced in 2017.

The beginning of 2018, though, showed that volatility is not dead and confirmed that the traditional strategies of ABC thrive in such conditions:

The start of 2018, especially February, further illustrates that the Group's strategies have the capacity to be very successful in normalized situations. The phase-out of "Quantitative Easing" and the programmed rate hikes during 2018 should provide for a more favorable market environment for the Group��s businesses.

(Source: company��s 2017 annual report)

As a small-cap stock, ABC Arbitrage is not required to release quarterly reports �� instead, they publish results on a semi-annual basis. Therefore, no first quarter earnings were released. Based on the higher VIX and comments from the company above, I assume Q1 was very strong, as with Virtu and Flow Traders (with the latter having its best quarter ever). H1 results will be released in September.

The good thing about underfollowed stocks like ABC Arbitrage is that they give investors who do follow the company an opportunity to position themselves before the market fully prices in the improving performance. In a conservative scenario where we get subdued volatility for the remainder of 2018, I expect the company to at least match 2016��s performance of ��30m net result, on the back on the strong Q1. This would equate to a 2018 P/E of 13 at current share price of ��6.9. With downside well-covered, investors get significant upside from exposure to a return of volatility.

ABC Arbitrage��s track record: EPS and distributionsThe historical performance of ABC Arbitrage's earnings is a testament to its correlation to volatility:

^VIX data by YCharts

^VIX data by YCharts2008 was the company��s best year ever as the great financial crisis unfolded (net result was ��40.6m). The first half of 2009 was very volatile as well. In 2011, the Eurozone's public debt crisis also created a fair amount of volatility, which benefited the company. As volatility receded in subsequent years, trading profits decreased, and ABC Arbitrage suffered from withdrawals from external clients resulting in lower assets under management. 2015 and 2016 showed gradual improvement before 2017 and its record low volatility took their toll on EPS. Because the company decided to maintain high payout despite the weaker 2017 earnings, part of the distribution was treated as repayment of capital contributions.

With regards to tax treatment, the general French withholding tax rate is 30%; however, there is a tax treaty in place between France and the US that lowers the rate for US investors to 15%, and those 15% are deductible from the investor��s US tax return.

Insider ownershipCEO Dominique Ceolin owns 16% of the company (either directly or via his 50.01% owned holding company Financi猫re WDD); David HOEY (deputy CEO) owns 5%, other managers own close to 4%. In 2017, the CEO purchased ��681k worth of shares.

Risks to considerAssets under management: in the outlook section of the 2017 annual report, the company signaled a decrease of AuM in early 2018, from ��434m as of end 2017 to ��384m as of March 1, 2018. Investors tend to get their timing wrong, leaving when volatility is low, and coming back when volatility has already returned. Withdrawals were probably the result of record low volatility in Q4, but I will be checking the next semi-annual report to see if the trend has reversed following the recent spike in volatility. Though external clients account for a lower share of revenue than proprietary trading, the company stated its intention to increase the size of AuM as part of the Step Up 2019 plan.

Technology risk: the company��s strategies rely on its proprietary algorithms. To remain competitive, ABC Arbitrage needs to keep its technological edge. The Step Up 2019 plan does include investments in technology. If, at some point, results did not respond to increasing volatility, that would be a warning sign.

TakeawaysIt is no coincidence that ABC Arbitrage had its best year in 2008, in the heat of the financial crisis. The company is a good way to get long volatility, and the VIX can be considered a leading indicator for its performance. The shares are up 10% YTD, but do not look expensive given the improved conditions in Q1, and there is potential for further appreciation if volatility returns for good. 2018 earnings should be sufficient to cover and possibly increase the distribution of close to 5.8% at current price.

Of course, there is no guarantee that the share price would not take a hit during a market melt-down, as investors throw the baby out with the bathwater. However, price action in February 2018, when the shares reacted well to the return of volatility, tends to show that investors have understood what drives the company's performance.

The most important thing is that in a downturn, operational performance would be strong, and the distributions would be well-covered and possibly growing (as happened in 2008 and 2009). Along with Virtu and Flow Traders, I think that ABC Arbitrage brings an antifragile component to a well-diversified portfolio.

Disclosure: I am/we are long FLTDF, ABC Arbitrage.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: The opinions and views expressed in this article are for information purposes only and should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation to buy, sell or hold any security, investment strategy or market sector.

24/7 Wall St.

24/7 Wall St.

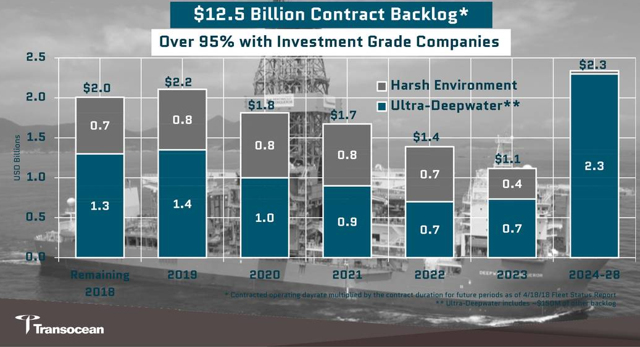

Source: Transocean, IHS Markit

Source: Transocean, IHS Markit Source: Transocean

Source: Transocean Source: Transocean

Source: Transocean Source: Transocean

Source: Transocean Pharmaceutical companies argue that they spend billions of dollars to research and develop new drugs, which they don’t want competitors profiting from by making cheaper generic copies of these medicines. These companies often fight for patent extensions, seek new uses for old products and sometimes prevent generic drug companies from obtaining samples.

Pharmaceutical companies argue that they spend billions of dollars to research and develop new drugs, which they don’t want competitors profiting from by making cheaper generic copies of these medicines. These companies often fight for patent extensions, seek new uses for old products and sometimes prevent generic drug companies from obtaining samples.