On Wednesday, May 16, 2018, offshore drilling giant Transocean (RIG) gave a presentation at the Citi Global Energy and Utilities Conference. While Transocean did spend a relatively small amount of time discussing the current conditions in the offshore drilling industry, the company devoted the majority of its efforts to discussing its own position in the industry as well as the methods that it has been using to weather the current downturn. Overall, the company has been handling the industry weakness quite well and will likely be positioned well when it finally recovers.

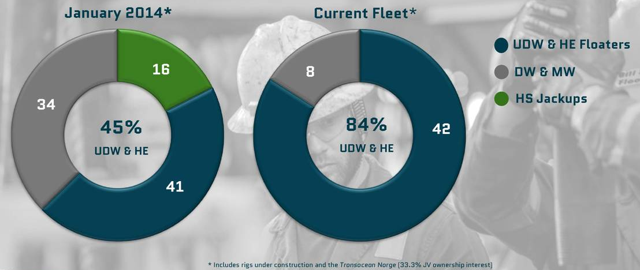

Transocean has long boasted one of the largest fleets in the offshore drilling industry, a status that it continues to hold to this date. With that said though, the company has somewhat changed the composition of its fleet over the course of the current downcycle. Here we see Transocean's fleet composition in January 2014 and today:

Source: Transocean

The current downcycle roughly began in the fourth quarter of 2013 so this does give us a good high-level overview of how the company has modified its fleet. As we can see here, when the downturn began, Transocean's fleet consisted of a combination of ultra-deepwater floaters, harsh-environment floaters, mid- and deepwater floaters, and high-specification jackup rigs. Since that time, the company has disposed of all of its shallow-water units and the majority of its mid- and deepwater units. The fleet shrunk substantially in the process.

This will likely prove to be a shrewd move for the company. As I have mentioned in numerous past articles, the exploration and production companies that make up the customers for the industry have been expressing a marked preference for securing the services of modern technically-sophisticated rigs. This has been true even throughout the downcycle, although the number of contracts being awarded was significantly lower than earlier this decade. As a general rule, most of the floating rigs that fall into this category are ultra-deepwater units. Midwater and deepwater rigs are generally older and certainly less capable than ultra-deepwater units. Thus, Transocean has streamlined its fleet to include the rigs that its customers are most interested in while reducing its deadweight, so to speak.

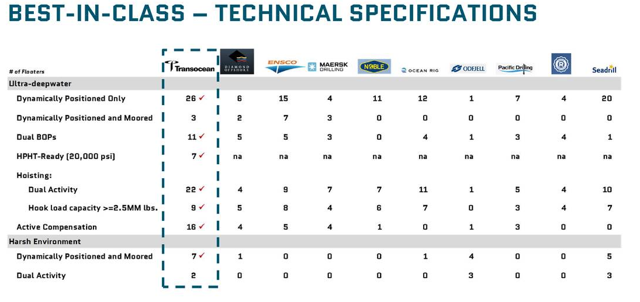

Transocean points this out in its presentation. As a direct result of the improvements that the company has been making to its fleet, it currently boasts the most advanced one in the industry.

Source: Transocean

Here we see that Transocean has more rigs with the features that customers have expressed interest or desire for than any of its major peers. The majority of these are items that will allow the rig to perform drilling operations in some of the demanding conditions that have become commonplace in today's market or safety equipment that reduces the risk of either worker injuries (and the ensuing costs) or the risk of oil spills and similar mishaps. This provides a competitive advantage for Transocean compared to its peers as it increases the likelihood that the company will have a rig available to meet the needs of a specific contract. Although this alone does not guarantee that the company will always win a contract, the chance is certainly increased.

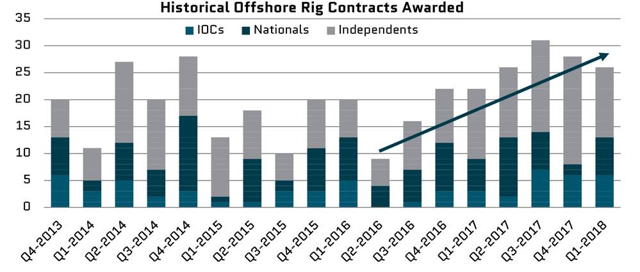

It is not exactly a secret that the ultra-deepwater segment of the industry has been struggling significantly over the past few years. this makes some sense. The downturn was originally precipitated by numerous exploration and production companies having strained cash flow due to high drilling costs, a problem that was exacerbated when oil prices collapsed in the middle of 2014. As ultra-deepwater rigs are by far the most costly type to operate and typically carried much longer contract terms than their shallow-water cousins, it makes sense that oil companies looking to save money would cut back on tendering ultra-deepwater rigs. Fortunately, that trend has begun to change since the beginning of 2017.

Source: Transocean, IHS Markit

Source: Transocean, IHS Markit

As we see here, the world's exploration and production companies are awarding significantly more floater contracts today than they were in 2015 or 2016, although the level is down slightly this year but this could be an effect of the harsh winter. It still bodes well for Transocean going forward however since a higher level of contract awards should result in the company's unemployed rigs receiving more contracts, which should improve Transocean's revenues and cash flows going forward.

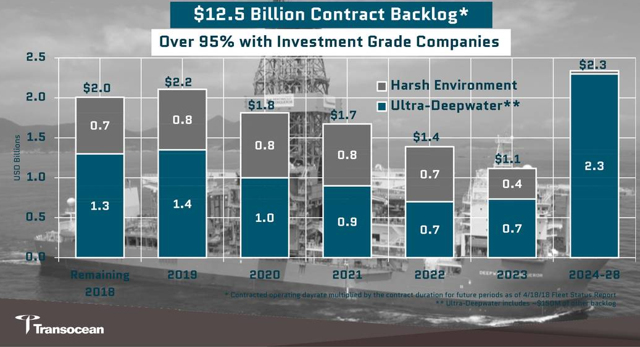

Transocean has already begun to see some benefits from this nascent recovery in the industry. As we see here, Transocean boasts an impressive $12.5 billion backlog:

Source: Transocean

Source: Transocean

This backlog is more than four times that of any of its nearest competitors.

Source: Transocean

Source: Transocean

A company's contract backlog is very important to an offshore drilling company. This is because it represents guaranteed revenues or at least as close as we can get to guaranteed in the industry as these future revenues are backed by contracts that the company has today. Thus, as investors we can use the company's backlog to get some idea of what a firm's forward revenues will look like. Here we can see that Transocean will bring in approximately $2.0 billion over the remainder of this year and $2.2 billion next year, with the amount steadily declining after that. It is worth noting that this is based on the company's current contracts so any new ones that it gets awarded will necessarily add to the amounts shown above.

Of course, as investors we are mostly concerned with a company's ability to turn its revenues into cash flow. Fortunately, Transocean has been able to accomplish this, even through the industry downturn. Here we see Transocean's revenue and EBITDA over the past three years:

Source: Transocean

Source: Transocean

As we can see here, Transocean's revenue declined 60% over the 2015 to 2017 period. Despite the decline, the company managed to convert its revenue into positive EBITDA in each of the three years, although it did understandably decline with the company's revenues. This is something that should clearly please investors as it shows that the company is able to generate profits for its owners in any market environment as the 2015 to 2017 period was one of the worst downcycles ever suffered by the industry.

One of the biggest disadvantages of Transocean's streamlined fleet structure is the absence of any shallow-water capability. As I explained in a recent article, the shallow-water market typically recovers significantly earlier than the ultra-deepwater sector and in fact this has happened over the past year. This is because the jack-up rigs that perform the drilling operations in this sector carry much lower dayrates than ultra-deepwater floating rigs. They also historically had shorter contract durations than their larger cousins, although that has changed somewhat in the past several months. In short though, shallow-water rigs represent less of a financial commitment than ultra-deepwater units. The lack of any of these rigs in its fleet will thus prevent Transocean from taking advantage of new opportunities in this sector and may slow its revenue recovery compared to some of its peers that possess jack-up rigs, such as Rowan Companies (RDC).

In conclusion, Transocean has done an admirable job weathering the industry downcycle. The company has streamlined and high-graded its fleet, which should position it well to take advantage of the eventual recovery in the ultra-deepwater industry while its large backlog should ensure that the company is able to produce cash flow for its investors while this story plays out. The company will, however, likely take longer to recover than some of its peers due to the absence of shallow-water units in its fleet.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

No comments:

Post a Comment